Credit unions have traditionally enjoyed a strong edge in member engagement over banks, but this advantage now seems to be dwindling.

Largely due to their not-for-profit-model, credit unions have had the upper hand on member (or customer) engagement compared to banks. While banks must be laser-focused on pleasing shareholders, credit unions have more flexibility to focus on member engagement and satisfaction.

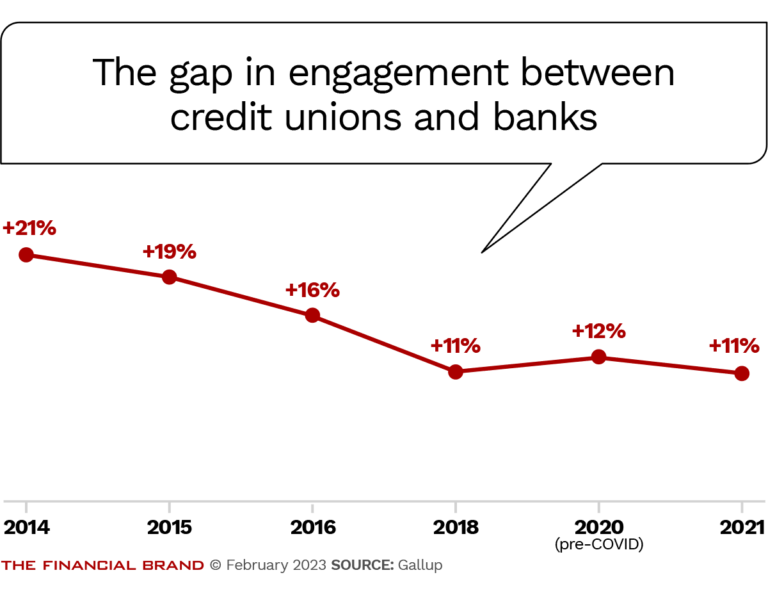

However, the gap between credit union and bank engagement appears to be narrowing. Gallup research shows that the engagement premium for credit unions versus banks has dropped from +21% in 2014, to only +11% today. NPS has also dropped from +29% to +17%

To turn the tide and help credit unions rebuild this foothold over banks, this will blog will explore:

Why credit union member engagement is so vital,

Why credit unions are losing their engagement edge over banks, and

What credit unions can do to improve member engagement quality and quantity.

Exclusive Webinar: Creating a Great Member Experience in a Finance-First State: A Fireside Chat with Del-One FCU

Why is credit union member engagement so vital

The competition for credit unions against banks is tough, particularly as banks continue to grow and invest heavily into digital transformation initiatives. In 2024, DragonFly Financial Technologies reported that 92% of banks plan to maintain or increase technology investment this year, with AI at the forefront of this strategy. JPMorgan Chase announced it planned to spend over $12 billion on technology in 2023, focusing on enhancing digital and mobile banking capabilities. Banks have also been reporting steady customer base growth. The retail banking market is forecasting a compound annual growth rate (CAGR) of over 5% between 2023 and 2032.

With this growing competition, any advantage that credit unions have over banks must be capitalized on. One such advantage has long been member-centricity. Being not-for-profit, the primary goal of credit unions is to serve their members, rather than maximize profits for shareholders. While they still need to make a profit, this fundamental difference should be emphasized to promote investment in member services.

The effects of enhanced credit union member engagement are palpable:

Purchase more products: Engaged members are more likely to invest in financial products offered by the credit union, and be more open to exploring additional products and services , such as loans and credit products.

Invest more capital: Engaged members are more likely to maintain higher deposit balances.

Remain a member for longer: Engaged members are more likely to build stronger relationships with their credit union, which plays a significant factor in their decision to stay with their credit union long-term.

Refer friends or family: Engaged members are more likely to engage in positive word-of-mouth and referrals, creating a highly effective customer acquisition channel.

However, the question facing many cooperatives today is; why is credit union member engagement dropping? And what can they do to turn the tide?

Why are credit unions losing their engagement edge over banks?

Credit unions have long prided themselves on having the upper hand when it comes to member, or customer, engagement. However, a recent study shows that this advantage is worryingly dissolving.

In 2014, credit unions enjoyed a +21% engagement premium over banks. They also achieved a +29% net promoter score (NPS). However, research now shows that both of these advantages have dropped. Credit union engagement premium now stands at +11%, with NPS crashing to only +17%.

There are many underlying reasons for this, some of which are beyond their control, and some that credit unions can and need to address.

One cause for lower credit union member engagement is the proliferation of buy-outs or mergers. The number of credit unions possessing less than $10 million in assets has plummeted from nearly 3000 to just over 1000 as cooperatives merged and consolidated. This has had significant impacts on member engagement. An advantage of credit unions compared to banks is their size – it’s typically easier for smaller credit unions with a smaller base to engage with their members on a more personal and community level.

However, there’s a more impactful and addressable reason for lower credit union member engagement – a widening in digital service offerings. Banks have responded more quickly and more extensively to a growing preference for digital financial services (stat on expenditure?). AI is central to this, with banks adopting voice and chat AI to improve engagement and deliver the convenience, instancy, and personalization that todays’ consumers expect.

Many credit unions are falling behind on this digital transformation. Perhaps even more concerning, many don’t believe it’s a pressing issue because of their member demographics. While it’s true that the average credit union member in the U.S. is 53 years old, studies show that this age profile is open to embracing new technologies. According to Fiserv’s 2023 report, 78% of Gen X (ages 44-59) consumers are comfortable managing their finances digitally, including making online payments, using mobile apps, and leveraging online financial tools.

As some credit unions delay, or even resist, digital financial services, they are both damaging engagement with current members, as well as alienating potential younger members.

How to improve credit union member engagement

Engaged members are the backbone of credit unions, so what can they do to both increase and improve credit union member engagement? Here are some of the most effective solutions that credit unions are finding success with today.

1. AI self-service that does more than FAQs

The pandemic accelerated the adoption of digital services by credit unions, but many still appear to not be wholeheartedly embracing the change. However, these institutions are resisting the inevitable.

While the average credit union member in the U.S. is 53 years old, this demographic is increasingly showing a preference towards digital support and service. 81% of Gen Xers are using online banking, and 66% use mobile banking apps. Moreover, these members aren’t just interested in digital services for simple needs – they want to use digital technologies for more complex queries too.

The first step towards this digital adoption should be to prioritize enhanced AI-driven self-service. In a somewhat surprising finding from a Certified Financial Planner Board of Standards’ survey, 62% of Gen X and Baby Boomers investors are satisfied using generative AI tools for advice, compared to just 38% of Millennial and Gen Z investors.

interface.ai’s voice, chat and co-pilot AI allow members to quickly and conveniently access support and have their queries resolved. Powered by domain-specific knowledge, multiple LLMs, and the industry’s most advanced proprietary Generative AI, interface.ai’s system can understand the nuances and complexity of both human and financial language. This translates into exceptional accuracy and resolution. Moreover, interface.ai’s hyper-intelligent AI can also help members complete complex tasks, such as managing accounts, accessing information, and making payments.

Great Lakes Credit Union launched interface.ai’s Voice Assistant and now experiences a 60-75% call containment rate – up from just 25% with their non-AI-powered IVR system. As Gallup put it: “Customers are shopping for conversation quality as much as they are shopping for products, services, rates and features, whether they know it or not.”

AI-self service also delivers the 24/7 availability that members appreciate and even expect. 85% of Gen X agreed that they ‘expect to interact with someone immediately when I contact a company.’ The convenience and intelligence of AI self-service enhances the overall member experience and keeps them more engaged with their credit union’s services. As Elizabeth Osborne, COO of GLCU explained at the U.S. Congressional hearing on AI Innovation in Financial Services:

“Our use of Olive [interface.ai] is a prime example of how the credit union industry can effectively deploy the use of AI to improve the lives of the members we serve.”

2. Personalization that shows that you care

In a report by Dynamic Yield on “The State of Personalization Maturity in Financial Services,” it was found that 92% of financial institutions plan to invest in digital personalization. So what is driving this interest in service and support personalization?

A banking study by Gallup identified that customers considered a high-quality conversation with a banker to be “needs-based, future-focused”. In other words, customers valued the banker’s understanding of their specific situation, what they needed from it, and how they could work towards it. Moreover, the study found that when a customer engaged in a high-quality conversation compared with a low-quality one, sales conversion was up to 4.2 times higher.

In another study, 80% of credit union members said they would like more personally tailored financial advice, while 21% would even consider moving credit unions to receive more personalized services. And if this wasn’t enough, another Gallup study showed that 73% of members who believed their credit union cared for their financial well-being were “engaged”, compared to only 20% for those who believed otherwise.

This perhaps shouldn’t be a surprise for credit unions. Their ultimate goal is to serve their members, and there’s no more impactful way for them to do so than helping their members achieve financial health.

To capitalize on this preference, and improve member engagement as a direct result, credit unions need to adopt technology that will allow them to provide tailored financial support and recommendations.

interface.ai’s Intelligent Banking AI is specifically built to provide exceptionally accurate and helpful personalized service for credit unions. The AI begins by analyzing vast amounts of cross-channel data, including customer interactions, transaction history, and behavior patterns. This comprehensive analysis provides a deep understanding of each customer’s needs and preferences. From here, the Chat AI can make proactive recommendations and helpful support based on the individual member’s financial situation, behavioral history, and previous conversations.

interface.ai’s Sphere for members takes this personalization even further. This industry-leading solution serves as a unified AI co-pilot to help members with all their online banking needs, from basic inquiries to complex transactions. Whether a member is asking for investment advice, checking their account balance, or looking for the nearest branch, the AI is ready with contextually relevant information tailored to the member’s preferences and past behaviors. To support the credit union’s mission to support their members financial wellbeing, Sphere can even guide members through complex financial topics, such as retirement planning or loan management, by offering personalized advice and educational content. This empowers members to make informed decisions that align with their unique financial goals.

These helpful, tailored recommendations significantly improve credit union member engagement. It shows a close understanding of each member, as well as a genuine interest in supporting their financial wellbeing.

This personalization across interface.ai’s solutions can also contribute towards cross-sell and upsell opportunities. Intelligent Banking AI can identify the optimal moments to present cross-sell and upsell opportunities. For example, if a customer is looking at a savings account, the AI might suggest a related investment product or premium account features at the right time, enhancing the chances of conversion. This is particularly valuable for credit unions who are having to move away from the success of in-branch cross-selling, providing an opportunity to showcase additional products in a digital setting.

Similarly, interface.ai’s Smart Conversion Chat AI can help guide members through application processes when they appear stuck. Smart Conversion proactively helps customers through applications with real-time support, pinpointing their issue and guiding them to completion. This also has a double benefit like Intelligent Banking. While the member receives relevant and personal assistance, the credit union can increase application conversion by 160%.

Wrap-up

While credit union member engagement has temporarily dropped, there’s much technological promise for it to improve again. Credit unions have access to the digital solutions they need to deliver the experience that members want – it’s just up to them to take the (proven to be successful) leap!

interface.ai provides the industry’s most advanced AI and Generative AI solutions to banks and credit unions to help them improve the banking experience while driving operational efficiency. Learn more about our Voice, Chat, and Co-pilot AI solutions.

In just 12 months, Chat AI has gone from “nice to have” to non-negotiable. A recent study shows a 57% surge in Chat AI adoption among credit unions with over $5 billion in…

For years, banks and credit unions have been promised “AI” that would transform service. But in reality, much of what’s been delivered are scripted bots in disguise. They look polished in a demo,…

{kind=link}